When I started out in financial services, I was on the front lines at the National Bank branch in Kilbirnie, Wellington. This was back in 2008. By then, ANZ had already acquired the National Bank in 2003, but it was still operating under its original name and branding. The black horse logo was iconic, and its sponsorship of the Black Caps gave it a strong presence in New Zealand sport.

It was a great place to learn. Back then, banks were part of everyday life. People came to deposit cash, pay bills, open accounts, and apply for loans. EFTPOS was common, but cash still mattered. On payday, queues stretched out the door. Businesses topped up their coins for change. Parents opened savings accounts for their kids. You’d help someone withdraw their first pay, then assist someone trying to cover a power bill. You saw the worry, the relief, and the quiet wins. It was a front-row seat to how money moved through real lives.

One of my earliest and most memorable interactions was with a customer I’ll call Rachel. She came in looking confused and a little embarrassed. Five months earlier, she’d bought a lounge suite and a washing machine for her flat using a store finance card that offered “12 months interest-free.” She was trying to avoid credit card debt and thought she was making the right decision. The salesperson had done a good job, and the deal sounded great.

But here’s the thing. Rachel was a second-year university student with a part-time job. And yet, she’d been approved for around $4,000 in financing. That was a lot back then. It all started when her first statement arrived. Rachel was blindsided. There were establishment fees, monthly account charges, and a repayment amount that seemed manageable at the time. But then her part-time hours were suddenly cut back following the Global Financial Crisis. What worried her most was the fine print. If she didn’t pay off the full balance before the end of the interest-free period, interest would be backdated from the time of purchase at nearly 30 percent.

To keep up with repayments, Rachel used her tertiary credit card to take out a cash advance. It had a $500 limit and was meant for emergencies. She didn’t realise that cash advances start accruing interest immediately, and at a much higher rate than regular purchases. There was also a cash advance fee, and no interest-free period applied.

But that’s not all – Rachel also had two bank overdrafts. One was a student overdraft with 0% interest, which was almost maxed out. The other was a standard overdraft that had started accruing interest. And not to mention her student loan.

You could see how she was starting to spiral. Not because she was reckless, but because she made a financial decision without fully understanding the consequences. On top of that, the lending rules were far too relaxed. Credit was easy to get, even for students with limited income. Once you’re caught in this kind of financial situation, it becomes harder and harder to regain control.

Rachel’s experience wasn’t unique. At the time, credit was easy to access, and the risks were often hidden. That’s why, in the years that followed, regulators began to take a closer look.

Seventeen Years On: What’s Changed?

Since then, lending rules have tightened. The Credit Contracts and Consumer Finance Act (CCCFA), first passed in 2003, saw major updates in 2014 and 2015. These changes introduced the Responsible Lending Code, which encouraged lenders to check whether a loan was affordable and suitable, and to clearly disclose the total cost, including interest, fees, and repayment terms.

The Code isn’t legally binding, but it provides guidance to help lenders comply with their legal duties under the law. It covers everything from how loans are advertised to how lenders should respond when things go wrong, like missed payments or repossession. Around the same time, new rules made it compulsory to publish interest rates, clearly display borrowing costs and include repayment warnings on credit cards.

More recently, some of these requirements have been relaxed. The aim was to make credit more accessible and reduce compliance pressure, especially for mainstream lenders. Whether that has made things better or worse is hard to say.

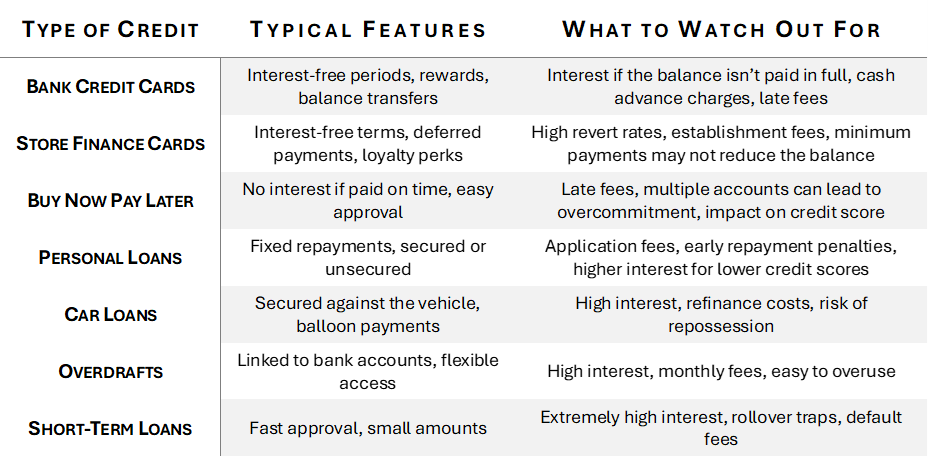

So, if you’re thinking about using credit today, it’s worth knowing what to look out for. Here’s a quick overview of common options and the traps that still catch people out.

Before You Borrow

This isn’t a deep dive into every product out there. It’s a simple overview of the types of credit people commonly use in New Zealand, along with key things to keep in mind.

If you’re considering any of these, take a moment to understand the full picture. Ask questions. Get clarity. And if something doesn’t sit right, it’s okay to walk away.

These products can be helpful, but they’re not risk-free. Credit is a tool. Like fire, it can warm your house or burn it down.

Before You Sign Anything

Credit can be useful, but it always comes with strings. Every product has terms, conditions, and consequences that aren’t always obvious.

So before signing up, ask yourself:

- What’s the real cost if I don’t pay it off in time?

- Are there fees or penalties I haven’t considered?

- Is this sustainable and necessary for my situation, now and for the future?

If you’re unsure, speak with someone you trust. Ideally, a qualified adviser or someone with real experience to help you see the full picture. Good advice at the right time can make all the difference.