In a recent financial education workshop for the Wāhine in Property Collective led by Cambridge Partners’ team of Hannah Meikle, Ashley Salt, and Anja Clarkson, one principle stood out clearly: successful investing isn’t about perfect timing—it’s about time. As markets experience volatility, understanding fundamental investment principles becomes even more crucial, especially for women looking to secure their financial futures.

Financial Planning: Your Foundation

Before diving into investment strategies, establishing solid financial foundations is essential. Financial Planning starts with self-reflection and goal setting. As Hannah explained, “When clients come in to see us, for the first half of the meeting, we don’t even talk about finances. We just want to get to know them as people and understand their goals and core values.”

This approach emphasises aligning your financial decisions with your personal values. For instance, Hannah shared how recognising family as a core value helped her budget for expensive flights home to the UK without stress. Understanding what truly matters to you creates a framework for meaningful financial decisions:

- Identify your short and long-term goals

- Clarify your personal values; this allows you to focus on aligning your spending and financial decisions with what matters most to you.

- Track expenses to understand your spending patterns and where you can make changes or create efficiencies. Being clear on your values and goals makes this easier.

- “Pay yourself first” by prioritising savings towards your goals before discretionary spending.

The Power of Long-Term Investing

Perhaps the most compelling insight shared was the extraordinary growth potential of long-term investing. Hannah illustrated this with a striking example: if a person had invested just $1 in the S&P 500 in 1927 and left it untouched, that dollar would now be worth several thousand dollars today. Significantly more than if it had been left in a savings account.

“Whilst we can’t predict the future, over the long term, markets have delivered great returns, and they are a fantastic way to grow long-term wealth,” Hannah emphasised.

This principle challenges the common misconception that small, regular investments aren’t worthwhile. Even modest contributions of $10-20 weekly can grow significantly over decades — a powerful message for those who feel overwhelmed by retirement planning, especially when juggling other financial commitments such as mortgages and raising a family.

KiwiSaver: Your Wealth-Building Engine

KiwiSaver emerged as a critical topic, with Ashley highlighting how KiwiSaver is now making up a significant portion of people’s wealth at retirement. Many participants had KiwiSaver accounts but hadn’t reviewed their strategy in years.

A concerning statistic revealed by Te Ara Ahunga Ora Retirement Commission found that women typically retire with retirement balances 25% lower than their male counterparts, largely due to the gender pay gap, career breaks and part-time work. To address this gap, Ashley suggested:

- Making voluntary contributions during career breaks (at least $1,050 annually to receive the full government contribution)

- Increasing contributions where possible, particularly if an employer matches the contribution

- Directing pay rises into KiwiSaver or other investments

- Regularly reviewing your KiwiSaver strategy to ensure it aligns with your risk profile.

“Your KiwiSaver is an investment,” Ashley reminded attendees. So, it’s something that you need to manage.” It’s a good idea to ensure you have the appropriate strategy, as this can make a big difference to your potential KiwiSaver balance in the future.

Navigating Market Volatility

With recent market turbulence making headlines, the Cambridge Partners team offered reassurance through evidence-based principles:

“Time in the market beats timing in the market,” Hannah stated firmly. This philosophy acknowledges that no one—not even financial professionals—can consistently predict market movements.

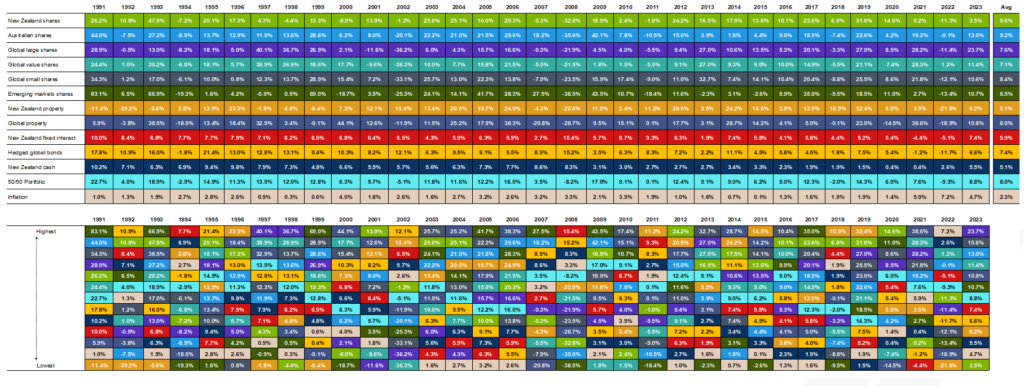

Anja reinforced this by showing a 30-year chart of asset class returns, demonstrating their randomness. “There is no way that you’re going to know what will do better next year versus the year before,” she explained. This chart visually represented the unpredictability of various asset classes over time. The seemingly random pattern of colours and numbers across the chart drove home the point that trying to pick winners year after year is futile.

The team cautioned against emotional reactions to market downturns, noting that those who switched to conservative funds during COVID-19 volatility missed the subsequent recovery and growth. Instead, they recommended:

- “Zooming out” to view long-term market trends rather than short-term fluctuations

- Maintaining appropriate diversification across asset classes

- Tuning out excessive market noise and media headlines

Interestingly, Anja noted that “women generally make better investors. We are a lot more considerate.” This natural tendency toward thoughtful, long-term thinking can be a significant advantage in wealth building.

Taking Action on Your Financial Future

Financial planning doesn’t require perfect knowledge or large sums to start. The Cambridge Partners team emphasised that beginning with small, consistent steps creates momentum toward financial security.

Whether reviewing your KiwiSaver strategy, starting a modest investment plan, or simply tracking your expenses, each action builds your financial foundation. As Hannah noted about her colleague who invested just $20 weekly: “If that’s what a dollar can do, if you invested just $20 a week for 5, 10, 15, 20 years, what does that look like?”

The answer, as the evidence shows, is potentially life-changing wealth over time—not through market timing or stock picking, but through patience, consistency, and the remarkable power of compound growth.